South Dakota has around ~54,000 residents enrolled in ACA exchange plans, 94% of whom are currently subsidized. I estimate they also have another ~3,000 unsubsidized off-exchange enrollees.

Green Mountain Care Board Receives 2026 QHP Rate Requests Amid Rising Health Care Costs

Montpelier, VT – On May 12, 2025, the Green Mountain Care Board (GMCB) received the 2026 individual and small group health insurance premium rate filings from BlueCross and BlueShield of Vermont and MVP Health Plan. The filings will be posted on GMCB’s rate review website. The average rate increases being requested are shown below:

Santa Fe, NM – The New Mexico Office of the Superintendent of Insurance (OSI) has approved 2026 rates for individual market Affordable Care Act (ACA) plans sold on and off BeWell, the New Mexico Health Insurance Marketplace, with an average increase of 35.7%. Today, 75,000 New Mexicans buy health insurance through BeWell and 88% of enrollees qualify for federal and state premium assistance.

However, there's an important caveat:

While it appears that Congress will allow enhanced federal Premium Tax Credits to expire, New Mexico’s Health Care Affordability Fund (HCAF) will cover the loss of the enhanced premium tax credits for households with income under 400% of the Federal Poverty Level (or $128,600 for a family of four), providing up to $68 million in premium relief for working families who enroll in coverage through BeWell in 2026. Federal and state premium assistance will continue to reduce the impact of the rate increases.

(Unfortunately, Avera hasn't provided a justification summary and has almost completely redacted their actuarial memo, making it impossible for me to know what their current enrollment is; see below)

Blue Cross and Blue Shield of Montana (BCBSMT) filed rates to be effective January 1, 2026, for its Individual ACA metallic coverage. As measured in the Unified Rate Review Template (URRT), the range of rate changes for these plans is an increase of 0.9% to an increase of 42.5%.

Product Blue Preferred Blue Focus Changes in allowable rating factors, such as age, geographical area, or tobacco use, may also impact the premium amount for the coverage.

There are currently 44,116 members on Individual Affordable Care Act (ACA) plans that may be affected by these proposed rates.

Consistent with the filed URRT, earned premiums for Individual plans during calendar year 2024 were $252,957,302 and total claims incurred were $235,192,937. The proposed rates effective January 1, 2026, are expected to achieve the loss ratio assumed in the rate development.

Blue Cross and Blue Shield of New Mexico (BCBSNM) is filing new rates to be effective January 1, 2026, for its Individual ACA metallic coverage. As measured in the Unified Rate Review Template (URRT), the range of rate changes for these plans is an increase of 18.4% to an increase of 49.6%.

The cost relativities among plans are different from the experience period to the prospective rating period due to anticipated non-uniform changes in network reimbursement levels. Additionally, the rates vary by plan due to the leveraging and utilization differences driven by variations in member cost sharing. Therefore, the proposed rates and rate changes may vary by plan.

Changes in allowable rating factors, such as age and geographical area, may also impact the premium amount for the coverage.

NJ Department of Banking and Insurance Releases Initial Health Insurance Rates for the Individual Market for Plan Year 2026

Federal Inaction on Enhanced Premium Tax Credits Among Issues Impacting Consumer Costs

TRENTON — The New Jersey Department of Banking and Insurance today announced that plan year 2026 health insurance initial rates have been submitted by insurance carriers operating in the individual market, which includes Get Covered New Jersey, the State’s Official Health Insurance Marketplace.

Plan year 2026 health and dental insurance rate filings, as proposed, are available for the companies listed below. These filings are subject to actuarial review. Additional companies will be listed as their filings are received. Any insurance filings already approved are available to the public through the NAIC’s System for Electronic Rate and Form Filing (SERFF) interface. There is no fee for using SERFF. Rate info can also be accessed at the Rate Review page at Healthcare.gov

AmeriHealth Caritas VIP Next, Inc:

Company Legal Name AmeriHealth Caritas VIP Next, Inc.

Market for which proposed rates apply (Individual or Small Group) Individual

Total proposed rate change (increase/decrease) 46.20% increase

Effective date of proposed rate change January 1, 2026

This actually came out a couple of weeks ago but ironically, I've been too swamped analyzing & posting 2026 rate filings for other states to get around to posting it here until now.

Overall preliminary rate changes via SERFF database, state insurance dept. website and/or the federal Rate Review database.

Hawaii Medical Service Association:

Our requested rates include only the amounts needed to cover the expected health care benefits of our members, the cost of administering their benefits, expected Affordable Care Act (ACA) fees, and a small charge to help manage the risk of offering benefits to this population.

We based our rate increase request on a review of past costs of benefits and other expenses. These historical costs are adjusted for trend, to account for expected changes in use of medical services, cost inflation, and other factors that affect the cost of care. We also adjusted costs for benefit changes, which were largely made to comply with government mandated plan designs. Administrative expenses have been relatively flat over the past couple of years.

Rate Watch is a convenient way for Hoosiers to access key data on Accident and Health rate filings submitted to the IDOI on or after May 1, 2010. Use it to determine which companies have requested rate changes, their originally requested overall % rate change, and the overall final % rate change approved. These are overall rate changes and are not individually specific. The table below is searchable and sortable. You can also download your filtered results by pressing the Save Excel File button at the bottom of the table. If you need the full data set, including a few additional columns, you can download the CSV file.

Vermont has around ~32,000 residents enrolled in ACA exchange plans, 93% of whom are currently subsidized. I estimate they also have another ~2,000 unsubsidized off-exchange enrollees.

Combined, that's ~35,000 people, although the official carrier rate filings claim it's more like 36,000 statewide.

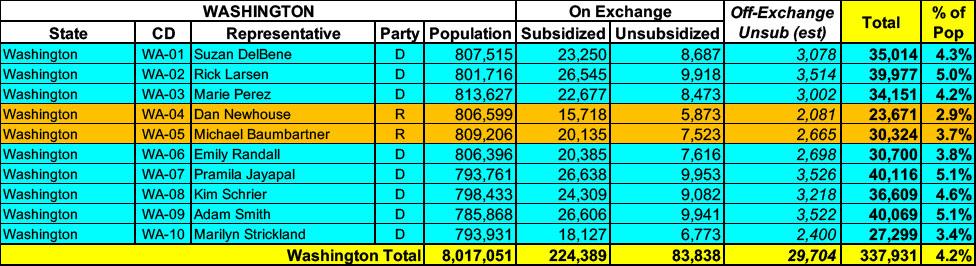

Washington State has around ~308,000 residents enrolled in ACA exchange plans, 73% of whom are currently subsidized. I estimate they also have another ~29,000 unsubsidized off-exchange enrollees.

Utah has around ~421,000 residents enrolled in ACA exchange plans, 95% of whom are currently subsidized. I estimate they also have another ~17,000 unsubsidized off-exchange enrollees.

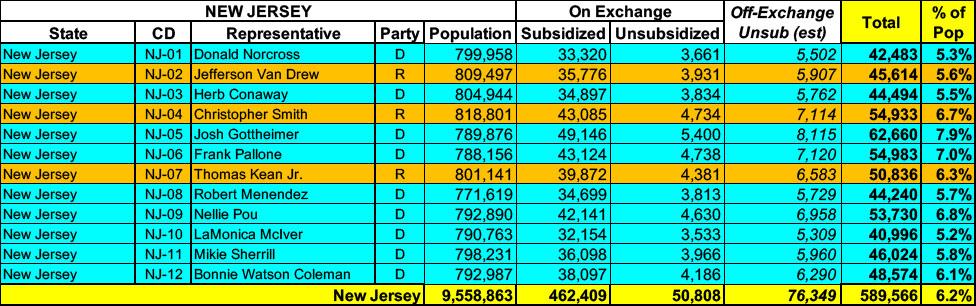

New Jersey has around ~513,000 residents enrolled in ACA exchange plans, 85% of whom are currently subsidized. I estimate they also have another ~76,000 unsubsidized off-exchange enrollees.

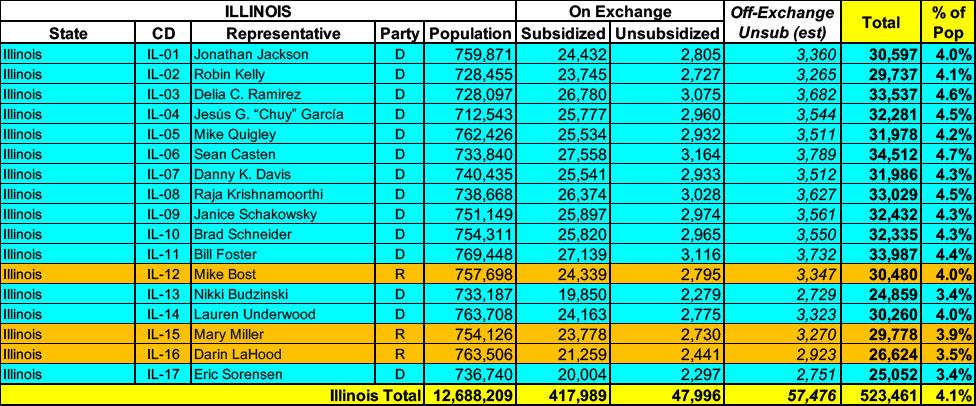

Illinois has around ~466,000 residents enrolled in ACA exchange plans, 90% of whom are currently subsidized. I estimate they also have another ~57,000 unsubsidized off-exchange enrollees.

Oregon has around ~140,000 residents enrolled in ACA exchange plans, 80% of whom are currently subsidized. I estimate they also have another ~34,000 unsubsidized off-exchange enrollees.

Oklahoma has around ~293,000 residents enrolled in ACA exchange plans, 93% of whom are currently subsidized. I estimate they also have another ~7,000 unsubsidized off-exchange enrollees.

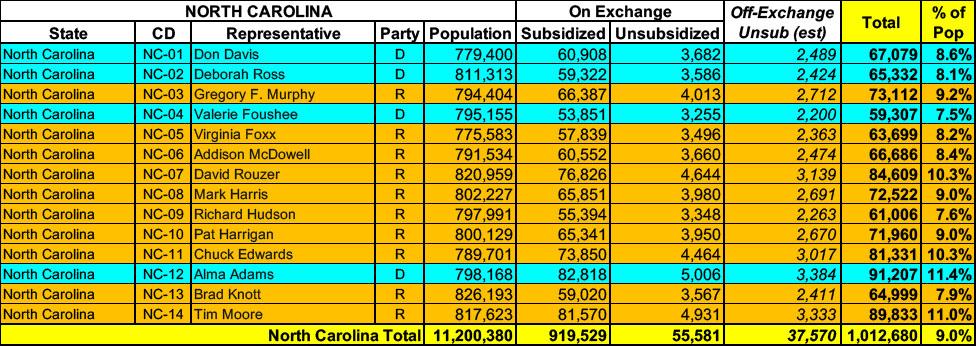

North Carolina has around ~975,000 residents enrolled in ACA exchange plans, 94% of whom are currently subsidized. I estimate they also have another ~37,000 unsubsidized off-exchange enrollees.

Montana has around ~77,000 residents enrolled in ACA exchange plans, 89% of whom are currently subsidized. I estimate they also have another ~8,400 unsubsidized off-exchange enrollees.

Louisiana has around ~293,000 residents enrolled in ACA exchange plans, 96% of whom are currently subsidized. I estimate they also have another ~13,000 unsubsidized off-exchange enrollees.

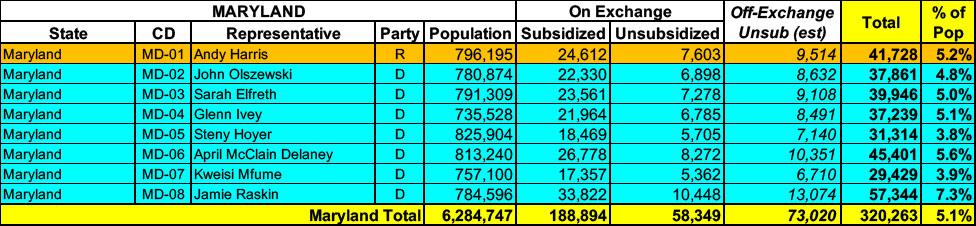

Maryland has around 247,000 residents enrolled in ACA exchange plans, 76% of whom are currently subsidized. I estimate they also have another ~73,000 unsubsidized off-exchange enrollees.

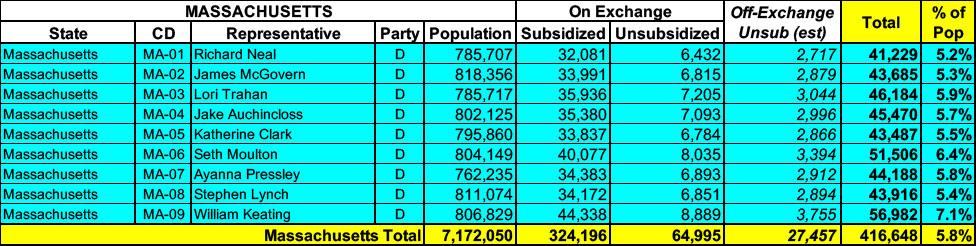

Massachusetts has around 390,000 residents enrolled in ACA exchange plans, 83% of whom are currently subsidized. I estimate they also have another ~27,000 unsubsidized off-exchange enrollees.

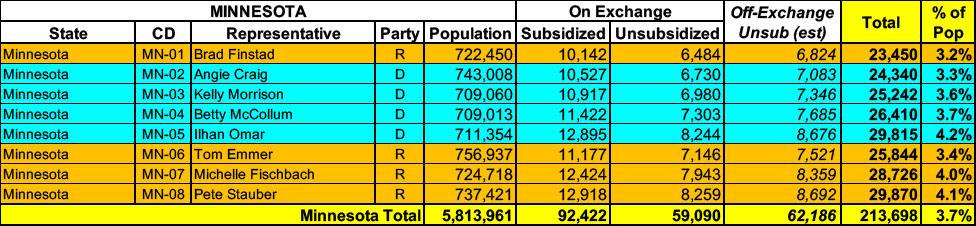

Minnesota has around 151,000 residents enrolled in ACA exchange plans, 61% of whom are currently subsidized. I estimate they also have another ~62,000 unsubsidized off-exchange enrollees.

Kentucky has around 97,000 residents enrolled in ACA exchange plans, 86% of whom are currently subsidized. I estimate they also have another ~6,800 unsubsidized off-exchange enrollees.

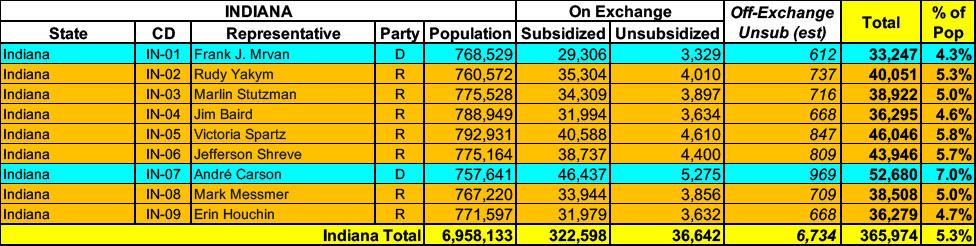

Indiana has around 359,000 residents enrolled in ACA exchange plans, 90% of whom are currently subsidized. I estimate they also have another ~6,700 unsubsidized off-exchange enrollees

According to the new report, total enrollment from September through December actually increased by just a hair (5,377) and still remained at over 20.7 million nationally, so it doesn't look like the Trump Admin has started cooking these particular books, at least not yet.

I've been able to cobble together more recent ACA expansion enrollment for about half of the 40 states (+DC) which participate in the program:

Hawaii has around 26,000 residents enrolled in ACA exchange plans, 83% of whom are currently subsidized. I estimate they also have perhaps another ~1,700 unsubsidized off-exchange enrollees.

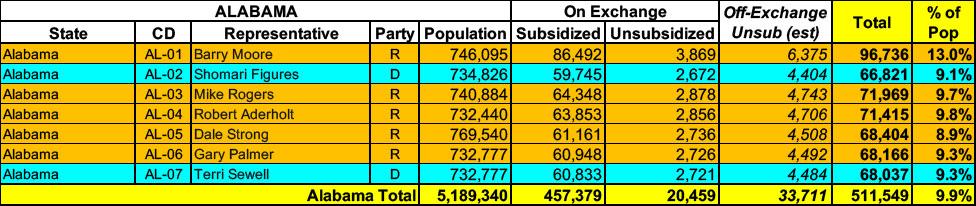

Alabama has around 477,000 residents enrolled in ACA exchange plans, 96% of whom are currently subsidized. I estimate they also have perhaps another ~33,000 unsubsidized off-exchange enrollees.

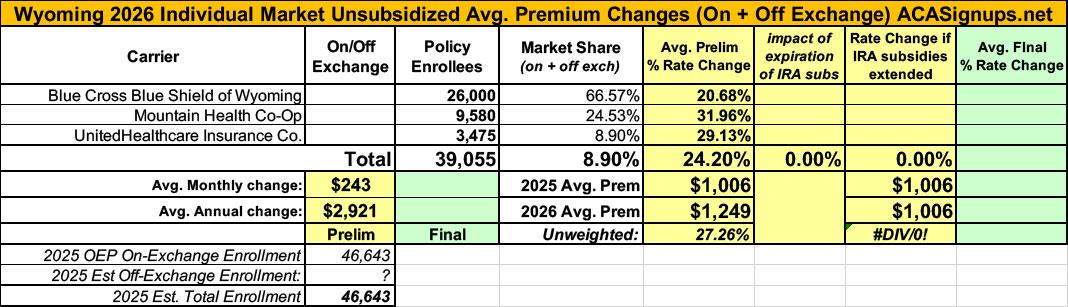

It was just a couple of weeks ago that the official (if preliminary) 2026 ACA individual market rate filings for Wyoming insurance carriers went live on the federal rate review website.

I published a writeup about these just 3 days ago; unlike some states, Wyoming was pretty easy to break out as they only have three carriers on the indy market, all of which also made their current enrollment data easy to find.

The landscape isn't pretty: BCBS is seeking average rate increases of 20.7%; UHC wants 29.1%, and Mountain Health Co-Op, which has around 9,600 enrollees, was asking for a whopping 32% average premium hike.

Keep in mind that Wyoming already has among the most expensive individual market policies in the country, with premiums averaging over $1,000/month.

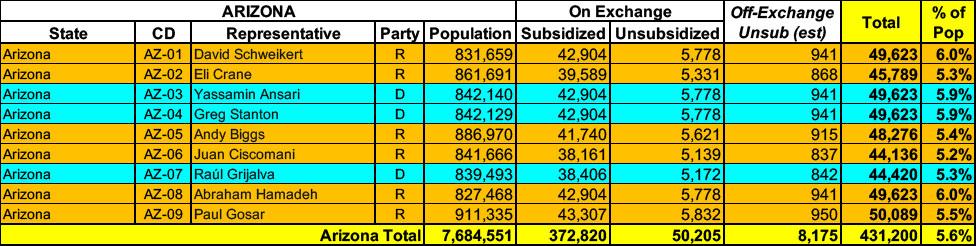

Arizona has around 423,000 residents enrolled in ACA exchange plans, 88% of whom are currently subsidized. I estimate they also have perhaps another ~8,000 unsubsidized off-exchange enrollees.

Open Enrollment Period through Get Covered New Jersey Begins November 1, 2025

TRENTON — New Jersey Department of Banking and Insurance Commissioner Justin Zimmerman today announced a total of $5 million in available grant funds for community organizations to apply to serve as state-certified Navigators for the Get Covered New Jersey Open Enrollment Period and throughout 2026. Navigators offer free, unbiased, community-based education and assistance to consumers seeking to enroll in health insurance through Get Covered New Jersey, the State’s Official Health Insurance Marketplace.

Delaware has ~53,000 residents enrolled in ACA exchange plans, 91% of whom are currently subsidized. They also have an unknown number enrolled in off-exchange plans. Overall, with net attrition, I estimate current total enrollment is down a bit to perhaps 52,000 today.

Connecticut has around ~151,000 residents enrolled in ACA exchange plans, 88% of whom are currently subsidized. I estimate they also have another ~7,000 unsubsidized off-exchange enrollees.

Whether the data posted since January 20, 2025 is accurate or not, I can't say for certain, but at least they're updating it...and so far, at least, I don't see anything in their monthly reports which is setting off any obvious red flags.

In any event, according to the latest report, as of April 2025: