Maine has around 64,000 residents enrolled in ACA exchange plans, 85% of whom are currently subsidized. I estimate they also have another ~4,500 unsubsidized off-exchange enrollees.

Combined, that's around 70,000 people, although it could be somewhat lower due to net enrollment attrition since January.

For months now I've been shouting from the rooftops about the imminent expiration of the improved federal tax credits for ACA enrollees, repeatedly pointing out that those already paying full price are gonna get hit with average premium hikes of over 23% while most of the 92% of exchange enrollees who currently receive at least some federal assistance will see their net premiums skyrocket by up to 100%, 200% or even 300% or more.

Having helped cause this crisis in the first place both by refusing to push Congressional Republicans to extend the enhanced subsidies as well as by changing the Premium Adjustment Percentage Index formula (PAPI) to make the remaining subsidies even less generous, the Trump Regime has come up with what I'm sure they think of as a brilliant "solution" to the problem.

Back in March I wrote about a proposed rule (really a set of rules) put out by the Trump Regime's Centers for Medicare & Medicaid Services (CMS) which, if implemented, would make major changes to how the Affordable Care Act is administered. This rule was finalized in June, with some provisions kicking in immediately, most starting January 1st and others over the next couple of eyars.

This set of regulatory changes is completely separate from the impending expiration of the improved premium tax credits which I've written so much about; these have to do with the specifics of how the ACA is actually implemented going forward.

A very simple example of this is the length of the annual Open Enrollment Period, which has ranged from as long as 6 months during the very first OEP in 2013-2014 to as short as just 75 days during most of the first Trump Administration.

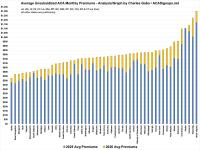

As I noted last month, Colorado's ~321,000 individual health insurance market enrollees are currently staring down the barrel of massive premium hikes less than four months from today:

Every state government is handling this situation differently. In Arkansas and New Hampshire, the strategy seems to be to either shout at or beg carriers to re-file with lower gross premium increases for 2026. New Mexico, California and New Jersey, in contrast, are all retooling their existing state-based supplemental subsidy programs to help cushion at least some of the impact.

For the individual market, this is actually slightly lower than the national average (23.4%), and New Hampshire will still end up with the 2nd-lowest avg. premiums in the country (Idaho should be slightly lower next year), but 22.4% is still pretty steep, and the state insurance dept. isn't happy about it:

New Hampshire Insurance Department Urges Health Carriers to Submit Revised 2026 Premium Rates Reflecting Current Economic Conditions

Every year, I spend months painstakingly tracking every insurance carrier rate filing (nearly 400 for 2025!) for the following year to determine just how much average insurance policy premiums on the individual market are projected to increase or decrease.

As of September 2nd, I've managed to fill in preliminary weighted average 2026 rate filings for all 50 states +DC as well as the final/approved rate filings for 15 states.

While it will move up or down slightly as more states finalize their 2026 filings, as of this writing, the weighted average rate increase for unsubsidized enrollees is 23.4% nationally.

This is the 2nd highest year-over-year gross rate hike since the ACA overhauled the individual market starting in 2014.

And yes, a significant chunk of this is due specifically to three factors:

Estimated Health Impacts of Almost $13 Billion Annually, Paralyzing Our Health Care System

1.5 Million New Yorkers Stripped of Health Care Coverage and Become Uninsured; Projected $8 Billion in Losses for New York’s Hospitals

Governor Kathy Hochul today joined U.S. Representative Ritchie Torres, local elected officials, doctors, and healthcare leaders to warn of the destructive ramifications of President Trump and Congressional Republicans’ “Big Ugly Bill” on New York State. The cuts imposed by Washington Republicans are expected to have a significant impact, with an anticipated nearly $13 billion affecting New Yorkers healthcare system. Additionally, approximately 1.5 million New Yorkers are projected to lose their health insurance coverage, while over 300,000 households are expected to lose some or all of their SNAP benefits.

Well this is a welcome bit of good news. While ACA major medical health insurance policy premiums are set to skyrocket in 2026 (largely due to Congressional Republicans allowing the improved premium subsidies to expire while the Trump Administration changes the underlying tax credit formula to make it significantly less generous), Covered California just announced that 2026 premiums for their standalone dental plans are set to cost pretty much the same next year:

Covered California Announces Premium Change for 2026 Dental Plans After Another Year of Steady Growth

SACRAMENTO, Calif. — Covered California announced that the statewide weighted average rate change for dental plans offered through the marketplace in 2026 will be 0.35 percent.

Overall preliminary rate changes via SERFF database, state insurance dept. website and/or the federal Rate Review database.

Anthem Health Plans of KY:

This filing includes an average rate change of 24.0%, excluding the impact of aging, effective January 1, 2026. At the individual plan level, rate increases range from 11.1% to 28.9% for renewing plans. A subscriber’s actual rate could be higher or lower depending on the geographic location, age characteristics, dependent coverage, and other factors.

Unfortunately, Anthem doesn't provide their actual 2025 individual market enrollment; I've had to estimate this based on marketwide estimated enrollment; see below.