The good news is that as of August 2nd, the preliminary 2020 ACA premium rate changes are now available for every state at the RateReview.HealthCare.Gov website.

The bad news is that while it does make it extremely easy to look up the average rate changes being requested for every carrier on the Individual and Small Group markets, they appear to have made it somewhat harder to dig up the other key data I need to run weighted averages...namely, the actual enrollment numbers for each, along with other noteworthy items like special circumstances, breakouts of the reasons for the rate changes and so on.

Every year some rate filing forms are redacted, but it seems to be more prevalent for 2020. I don't know if that's something being done by the carriers or at HC.gov's end, but for whatever reason, it's more difficult for me to run weighted averages this year.

Over the past year or so, ever since Donald Trump issued an executive order re-opening the floodgates on non-ACA compliant "short-term, limited duration" (STLD) healthcare policies (otherwise known as "junk plans" since they tend to have massive holes in coverage and leave enrollees exposed to financial ruin in many cases), numerous states have passed laws locking in restrictions on them or, in a few cases, eliminating them altogether:

The final unsubsidized rates are down about one point more, down 6.3% from 2018 rates. However, as all three current carriers clearly noted in August, the repeal of the ACA's individual mandate and expansion of short-term and association health plans (aka #ShortAssPlans) still caused a significant premium increase, which means without those factors, 2019 rates would likely be down significantly more...likely nearly 20% instead of 6.3%:

Arizona has only three carriers offering individual market policies next year. Blue Cross Blue Shield of AZ has nearly 40,000 enrollees and is keeping rates virtually flat, but specifically states that yes, they baked in extra costs to account for Congressional Republicans repealing the ACA's Individual Mandate and due to Trump's expansion of #ShortAssPlans (see screenshot below).

Centene is dropping rates by over 5 points. I don't know their exact enrollment/market share, so I'm forced to assume it's similar to last year's 95,000. Again, they call out both #MandateRepeal and #ShortAssPlans, but don't include a specific percentage for either (they did, but it was redacted in the public filing).

Finally, Cigna is dropping their 2019 premiums by a whopping 18.2% even with sabotage factors, which again are referenced in the filing. I don't know their enrollment either, but amd assuming it's roughly 16,000 since Arizona's total ACA indy market is around 150,000 people.

To the best of my knowledge, there are only 2 insurance carriers offering ACA-compliant insurance policies in Arizona next year: Blue Cross Blue Shield of AZ and Centene (branded as HealthNet).

Back in early August, BCBSAZ announced that they were asking for a relatively modest 7.2% rate increase next year in the 13 counties (out of 15 total) where they were offering individual plans. They also explicitly stated that if it weren't for their concerns over whether or not the Trump Administration would guarantee reimbursing their CSR expenses, they'd be keeping the 2018 rates flat year over year. Granted, this is after a massive rate increase for 2017, but it was still welcome news, and once again underscored how much damage the Trump sabotage factor is.

This isn't a full analysis, since I only have 2018 rate hike data for one of Arizona's carriers so far...on the other hand, AZ only has a couple of carriers on the individual market these days anyway. From AZCentral:

The Affordable Care Act insurer in 13 of Arizona's 15 counties plans to raise average rates across all plans a moderate 7.2 percent next year.

But Blue Cross Blue Shield of Arizona officials said the rate increases would be flat if President Donald Trump's administration did not plan to eliminate a key Affordable Care Act funding source.

7.2% isn't bad at all...of course, that comes after last years massive 57% average rate hike. Still, 0% would obviously be much better than 7%...

Trump suggested in a weekend tweet that " ... bailouts for insurance companies and bailouts for members of Congress will end very soon" unless Congress acts quickly on a new health bill.

Of the 31 states which have expanded Medicaid under the Affordable Care Act, only a handful issue regular monthly or weekly enrollment reports.

I noted in February that enrollment in the ACA's Medicaid expansion program had increased by around 35,000 people across just 4 states (LA, MI, MN & PA).

It's early June now, so I checked in once more, and the numbers have continued to grow. I have the direct links for 5 states now (including New Hampshire)...

OK, this appears to be quickly turning into my next project thing. The methodology here is pretty much the same as the other states; the only major difference is that while I do know the total Medicaid enrollment for each county (as of December 2016), I don't have that broken out between traditional and expanded Medicaid. Fortunately, I have a hard state-wide number for that: Around 398,000, or roughly 20.8% of the state-wide total. I've therefore multiplied each county number by 20.8% to get a rough estimate of the ACA expansion tally for each.

Like Texas, I'm also no longer expecting Arizona to beat last year's Open Enrollment total by much. Assuming 209K QHP selections, there should be around 125K indy market enrollees and 399K Medicaid expansion enrollees who'll be in a world of hurt post-repeal, or roughly 524,000 altogether.

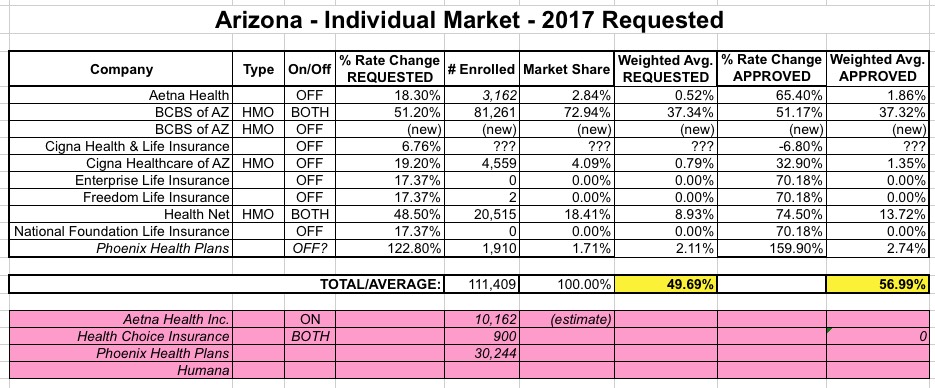

The ACA exchange in Arizona has hadsome prettydramaticturns over the past month or so. When the dust settled, every county in the state will still have at least one carrier offering plans on the exchange...although only one. Anyway, today the AZ DOI joined Pennsylvania and Michigan in releasing their final approved rate hikes for both the individual and small group markets: